Adaptio vs VC-Backed GTM: Which Growth Model Wins in 2026?

Adaptio (capital-efficient, adaptive growth) versus the VC-backed blitzscale playbook. A neutral breakdown of cost, speed, risk, and which model fits your 2026 go-to-market.

TL;DR

- Adaptio is the capital-efficient, adaptive growth model: spend tied to proven unit economics, slow-but-durable expansion, founder-led GTM. VC-backed is the blitzscale model: raise big, hire ahead of revenue, buy growth and market share before profitability.

- Neither model is "correct." The right one depends on your market size, payback period, and how defensible your category is.

- VC-backed wins when the market is winner-take-most and speed creates a moat. Adaptio wins when payback is long, churn is real, and capital is expensive (which it is in 2026).

- Most durable companies in 2026 run a hybrid: adaptive discipline on cost structure, selective VC fuel on the one or two motions with proven payback.

- Whatever model you pick, GTM efficiency starts with clean data and accurate targeting — the cheapest lever either model has.

What does "Adaptio vs VCBacked" actually mean?#

Short answer: it's a debate about how you fund and pace go-to-market, not about which CRM you use.

Think of two ways to fill a swimming pool. The VC-backed way is to rent the biggest pump you can find, run it at full power, and accept that you'll spill water everywhere as long as the pool fills before your competitor's. The Adaptio way is to match the inflow to how fast the pool can actually hold water without cracking — slower, but you never blow a seal.

In business terms:

- Adaptio describes an adaptive, capital-efficient growth model. You grow by reinvesting revenue and small, disciplined capital, you keep burn close to break-even, and you scale a motion only after its unit economics are proven. Spend adapts to evidence.

- VC-backed describes the venture-funded blitzscale model popularized over the last decade. You raise a large round, hire sales and marketing ahead of demand, and prioritize market share and growth rate over near-term profitability, betting that scale will produce a moat later.

This isn't a brand-versus-brand review. It's a strategy comparison — and in 2026, with higher interest rates and a tougher fundraising climate, the trade-offs have shifted meaningfully versus the 2019 playbook.

How do the two growth models compare?#

Here's the head-to-head on the dimensions that actually move the decision.

| Dimension | Adaptio (capital-efficient) | VC-Backed (blitzscale) |

|---|---|---|

| Primary fuel | Revenue + small raises | Large equity rounds |

| Burn target | Near break-even | High, intentional |

| Hiring pace | Behind proven demand | Ahead of demand |

| Decision driver | Unit economics evidence | Growth rate / market share |

| Payback tolerance | Short (under 12 mo preferred) | Long (18–24+ mo acceptable) |

| Dilution | Low | High |

| Failure mode | Growing too slow, missing the window | Running out of runway before the moat |

| Best for | Long-payback, churn-prone, niche markets | Winner-take-most, network-effect markets |

| Control | Founder retains | Board / investor influence grows |

| 2026 fit | Strong (expensive capital) | Selective (top decile only) |

Notice there's no "winner" row. That's deliberate — the column that wins flips entirely based on your market structure, which we'll get to.

Is Adaptio better than the VC-backed model?#

Conclusion first: Adaptio is the safer default in 2026, but it is not universally better. It's better in the conditions that describe most B2B software companies today, and worse in a small set of high-velocity, winner-take-most categories.

Adaptio wins when:

- Payback periods are long. If it takes 14 months to earn back customer acquisition cost, burning hard just multiplies your exposure if retention slips.

- The market is fragmented. No single player will own it, so racing to "win" the category is spending money to win a prize that doesn't exist.

- Capital is expensive. In a high-rate environment, every dollar of dilution or debt costs more. According to Bessemer Venture Partners' State of the Cloud research, efficiency metrics like the "Rule of 40" have become the dominant lens investors apply — growth at any cost is out of fashion.

- Churn is non-trivial. Blitzscaling a leaky bucket just pours more water through the holes.

The catch: Adaptio can be too slow. If a venture-funded competitor locks up distribution, integrations, and brand while you're being disciplined, you can win every unit-economics argument and still lose the market. Discipline that misses the window is just a well-documented failure.

When does the VC-backed model actually win?#

The VC-backed model earns its dilution in a specific shape of market: winner-take-most categories with real network effects or strong switching costs, where being first to scale creates a durable moat.

Marketplaces, infrastructure standards, and viral collaboration tools are the classic examples. In those categories, the second-place finisher with great margins is still a footnote. Speed is the strategy, and the capital buys the one thing you can't earn back later: time.

VC-backed also wins when:

- The opportunity is genuinely large and time-boxed — a platform shift (AI being the obvious 2026 example) that won't stay open.

- You have a credibly defensible wedge that gets stronger with scale (proprietary data, network effects, ecosystem lock-in).

- You can actually deploy the capital efficiently. Money doesn't create demand; it amplifies a working motion. Pouring fuel on an unproven funnel just burns faster.

The failure mode is well known: companies raise big, scale a motion that never had healthy payback, and hit the wall when the next round doesn't materialize at the valuation they need. The graveyard of 2022–2024 down-rounds is full of teams that confused fundable with viable.

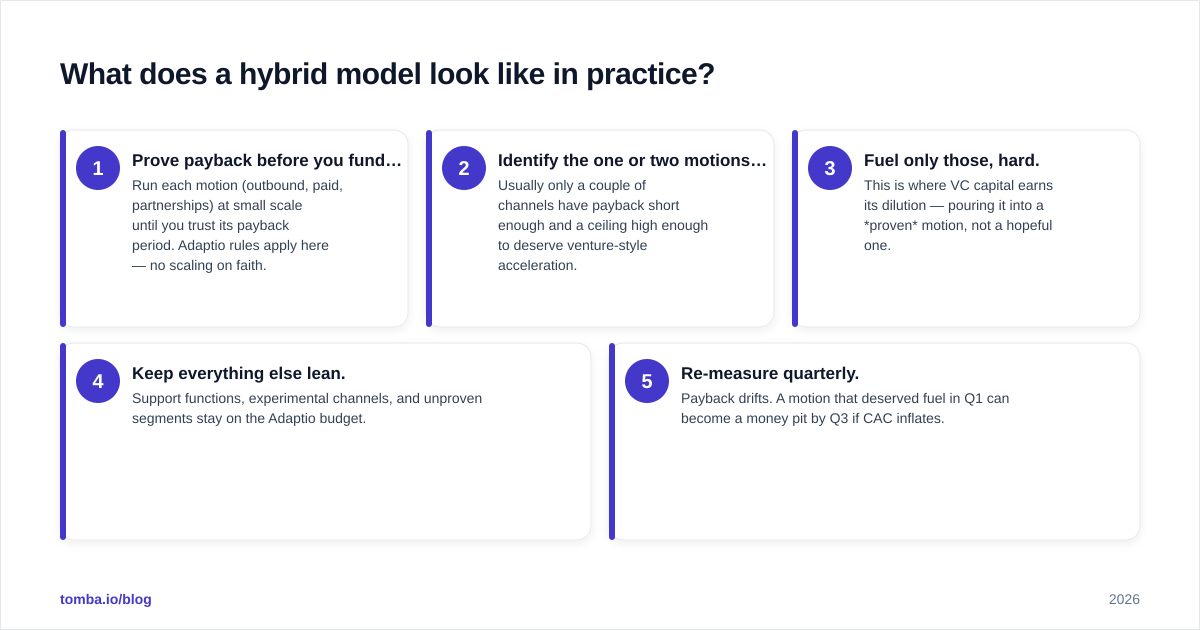

What does a hybrid model look like in practice?#

Most of the durable companies in 2026 aren't purists. They run adaptive discipline on the cost structure and selective VC fuel on the proven motions. The framework below is how operators actually decide where to spend.

The decision sequence:

- Prove payback before you fund it. Run each motion (outbound, paid, partnerships) at small scale until you trust its payback period. Adaptio rules apply here — no scaling on faith.

- Identify the one or two motions worth fuel. Usually only a couple of channels have payback short enough and a ceiling high enough to deserve venture-style acceleration.

- Fuel only those, hard. This is where VC capital earns its dilution — pouring it into a proven motion, not a hopeful one.

- Keep everything else lean. Support functions, experimental channels, and unproven segments stay on the Adaptio budget.

- Re-measure quarterly. Payback drifts. A motion that deserved fuel in Q1 can become a money pit by Q3 if CAC inflates.

This is essentially the "Rule of 40" applied at the motion level instead of the company level: each channel earns its capital by clearing a combined growth-plus-efficiency bar.

How does data quality change the math for both models?#

This is the part both camps underrate. The cheapest way to improve unit economics — in either model — is to stop wasting spend on bad targeting and bad data.

Acquisition cost is a fraction with two levers: what you spend, and how many of the right people you reach. Most teams obsess over the first and ignore the second. If 30% of your prospect list is wrong-fit, undeliverable, or stale, you're inflating CAC by 30% before a single rep makes a call — and that inflation is exactly what kills the VC-backed model and slows the Adaptio one.

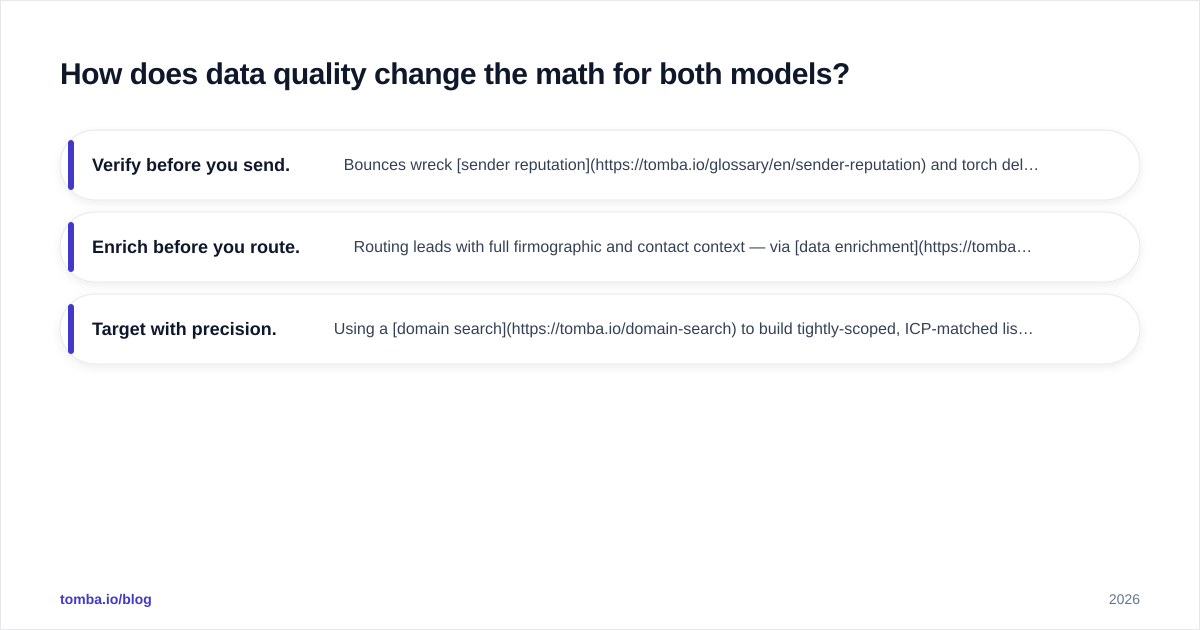

Concretely:

- Verify before you send. Bounces wreck sender reputation and torch deliverability, which silently raises the cost of every future campaign. An email verifier step before outreach is one of the highest-ROI process changes either model can make.

- Enrich before you route. Routing leads with full firmographic and contact context — via data enrichment — means reps spend time selling instead of researching, which shortens payback directly.

- Target with precision. Using a domain search to build tightly-scoped, ICP-matched lists beats buying a giant generic database that you then pay to clean.

For the Adaptio team, clean data is how you hit short payback without a war chest. For the VC-backed team, it's how you make sure the fuel you're pouring actually lands on demand instead of evaporating. Same lever, both playbooks.

What metrics should you actually watch?#

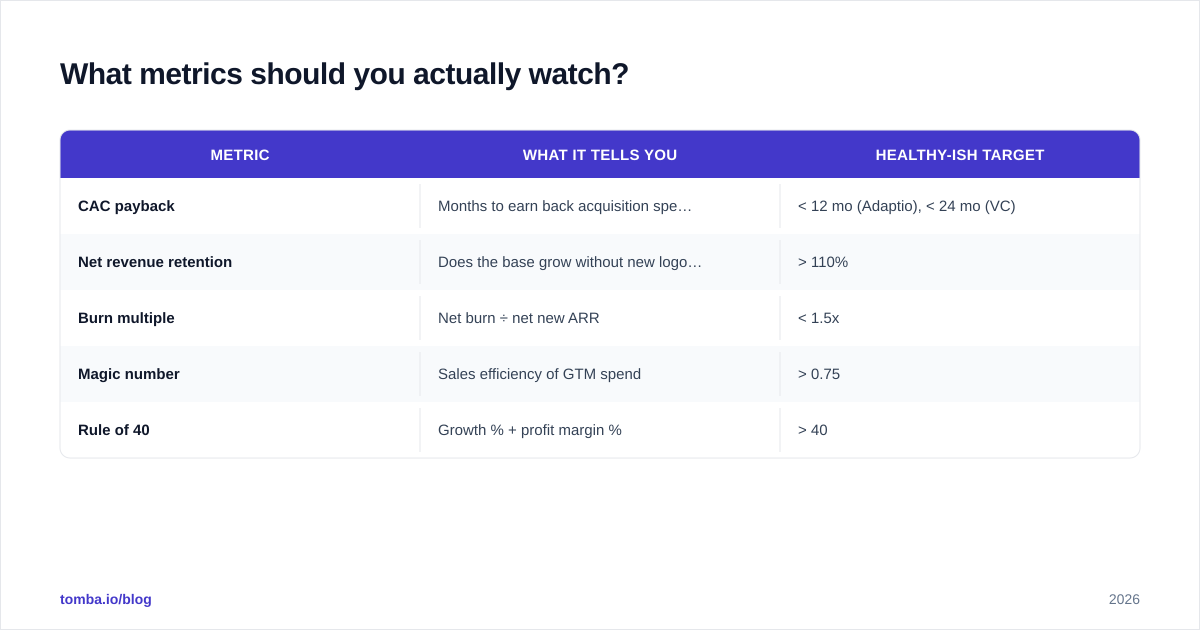

Skip vanity metrics. Both models live or die on a small set of numbers:

| Metric | What it tells you | Healthy-ish target |

|---|---|---|

| CAC payback | Months to earn back acquisition spend | < 12 mo (Adaptio), < 24 mo (VC) |

| Net revenue retention | Does the base grow without new logos? | > 110% |

| Burn multiple | Net burn ÷ net new ARR | < 1.5x |

| Magic number | Sales efficiency of GTM spend | > 0.75 |

| Rule of 40 | Growth % + profit margin % | > 40 |

If your burn multiple is above 2x and your NRR is under 100%, no amount of fundraising fixes the underlying motion — you're scaling a problem. If your Rule of 40 is comfortably above 40 and you're starving growth out of caution, you may be leaving a winner-take-most window open for a competitor. Read the numbers before you read the pitch decks. Industry benchmarks from sources like Gartner's go-to-market research and public SaaS comps give you the goalposts.

Which model should you choose for 2026?#

Decide with three questions, in order:

- Is your market winner-take-most? If genuinely yes — network effects, standards, marketplace dynamics — lean VC-backed and move fast. If no (most B2B SaaS), lean Adaptio.

- Is your payback under 12 months on at least one motion? If yes, you've earned the right to consider fueling it. If no, fix the motion before you fund anything.

- How expensive is your capital right now? In 2026's rate environment, dilution is costly. The bar for "worth raising" is higher than it was in 2021.

The honest default for the median B2B company in 2026 is Adaptio with surgical VC fuel — run lean, prove payback, then accelerate the one or two motions that clearly clear the bar. Pure blitzscale is a top-decile strategy for genuinely time-boxed, winner-take-most opportunities. Pure bootstrapping can leave a real market on the table. The hybrid is where most winners live.

Bring efficiency to whichever model you run#

Whether you're running lean by necessity or fueling a proven motion with venture capital, your go-to-market is only as efficient as the data underneath it. The fastest way to cut wasted spend in either model is to make sure every contact you pay to reach is real, current, and on-ICP.

Tomba's Email Finder lets you build precise, verified prospect lists by domain, name, or company — so your CAC reflects real demand, not bounced sends and bad routing. Start on the free tier (25 searches a month) to pressure-test your targeting, then scale into a paid plan as your motion proves out. Check the full Tomba pricing to match a tier to your stage. It's the one investment that pays back the same way under both the Adaptio and the VC-backed playbook: less waste, shorter payback, more durable growth.

Get the Tomba newsletter

Practical outbound tactics and product updates — once every two weeks.

About the author